Key terms in this blog:

- Credit score: Predicts how likely a person will pay a loan back over time.

- Debt consolidation: Combining multiple debt payments into one may be a way to simplify or lower payments.

- Annual Percentage Rate (APR): Standard way to compare how much a loan costs.

Looking to purchase a home or maybe a new car? Unless you intend to pay for these big-ticket items in cash, you’re likely going to need a good credit score. Debt consolidation are two words that can help.

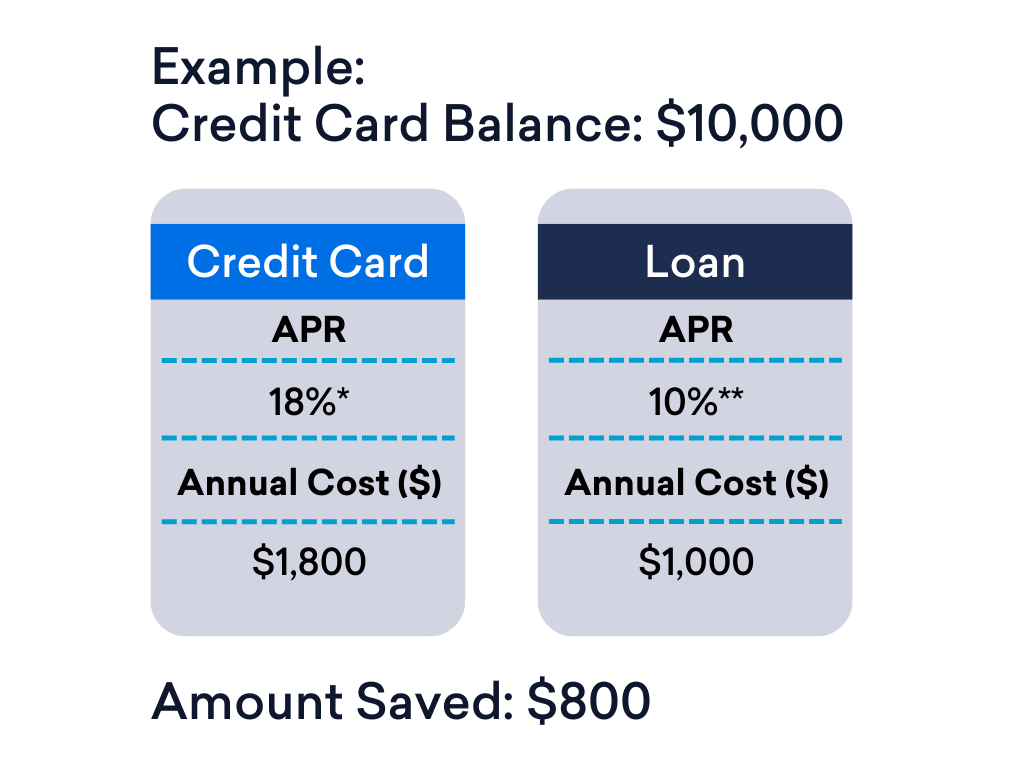

Why consolidate debt? Short answer is you could save money on interest paid and reduce your overall debt.

Ways to consolidate debt:

- Personal loans: Usually offer lower interest rates, in some cases as low 10%**.

- Balance transfers: Transfer higher balances to credit cards with lower interest rates.

- Retirement account loans: You may be able to take a loan from your retirement account.

- Home equity loan or line of credit: You may be able take a loan against the value of the portion of your home that you own

How debt consolidation can improve your credit score:

- Lower credit utilization ratio: Measures how much of your available credit you are using. By adding a debt consolidation loan, you increase your available credit. Provided you don’t add more debt, your credit utilization ratio will decline which is good for your credit score.

- Improved payment history: Payment history is a key to a good credit score. By consolidating multiple payments with a higher interest rate into one with a lower interest rate, it may be easier to make payments.

For more info on this, check out: How does debt consolidation affect my credit scores?

Get the Beanstox App

Download the app.

We’ll help you set up recurring investments into a portfolio that fits your financial goals. It’s Seriously Simple Investing.